Normally, when a currency is falling, a simple step exists to revive it: raising interest rates. But in Hong Kong there are no interest rates to raise, and that’s created problems.

Hamstrung because it ceded monetary policy to the U.S. Federal Reserve 35 years ago, the Asian financial hub has had no choice but to watch as a decade of radical stimulus by a foreign central bank sent money coursing across its borders. The inflows have jacked up prices on everything from apartments to car park spaces.

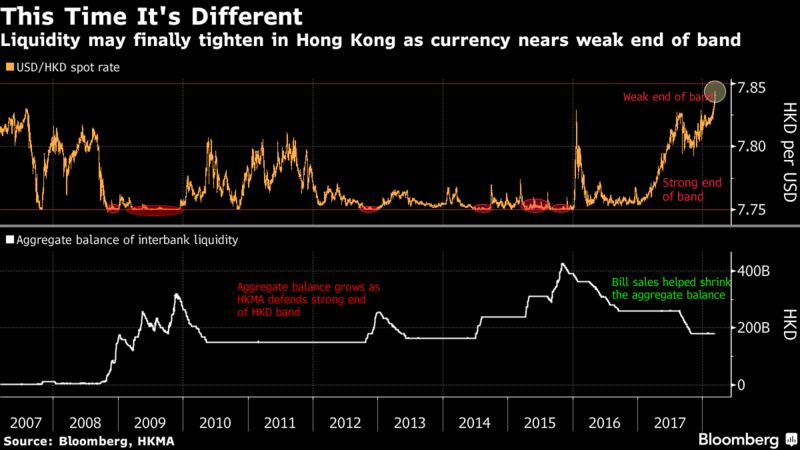

The situation is on the verge of boiling over: Hong Kong’s dollar has weakened to a point where intervention is about to become obligatory. And to politicians and anyone else concerned about asset bubbles in the city, it couldn’t be happening at a better time.

“Why have home prices risen non-stop for 10 years? It’s not related to the economy. It’s a purely monetary phenomenon,” said Raymond Yeung, an economist at Australia & New Zealand Banking Group Ltd. in Hong Kong. “If Hong Kong rates don’t rise, it’s hard for asset prices to correct.”

When the currency reaches the weak end of its band against the greenback, the Hong Kong Monetary Authority will be compelled to buy Hong Kong dollars, thereby sucking up liquidity — and finally lifting interbank rates that are lagging behind their U.S. equivalents. The widening rate discount is why the currency has been falling.

The HKMA pushed the Hong Kong dollar further in that direction on Thursday when it issued a statement ruling out issuing additional bills — sales that previously have helped lift the exchange rate. The currency fell as much as 0.1 percent after the comments, its biggest decline since December. The Hong Kong dollar last traded at HK$7.8378, within 0.16 percent of the HK$7.85 level that marks the weak limit of the peg.

When the HKMA steps in to defend weak end of the band, the monetary base will shrink gradually, allowing local rates to normalize, said Norman Chan, head of the HKMA. One-month Hibor is more than 100 basis points below the U.S. equivalent of Libor, the biggest spread since 2008.

The market started pricing in expectations for higher rates after the HKMA’s statement. Twelve-month forward points surged the most since December 2016 that day, and one-year interest-rate swaps extended a nine-year high on Friday. The one-month interbank rate known as Hibor rose the most since Dec. 1.

With reserves of $443.5 billion, the HKMA is not short of ammunition. Once intervention begins, the pace can be sizable. Back in 2004, when rates were similarly lagging behind during a period of Fed hiking, the HKMA bought $4.1 billion worth of Hong Kong dollars over two months, helping drive the one-month Hibor up 86 basis points.

There’s plenty of cash to absorb. The city’s aggregate balance of interbank liquidity is still 100 times pre-crisis levels. It may also take a substantial increase in rates to knock the housing market off course. But the risks from a sustained period of easy monetary policy in a buoyant economy are mounting. In the Bank for International Settlements’ measure of the deviation of an economy’s credit-to-gross domestic product ratio from its long-term trend, Hong Kong came first in the world among 44 economies tracked, indicating unusually rapid debt growth in recent years.

“The HKMA is willing to take the risk to show the rest of the world the Hong Kong currency board can withstand depreciation pressure,” said ANZ’s Yeung. “We’ve seen inflows for many years, but very seldom do we see outflows.

Source:BLOOMBERG

You may also like

-

Xiaomi Makes Its Trading Debut on the Defensive

-

U.S. Pulls Trigger on China Tariffs, Sparking Vow of Retaliation

-

China Vows Not to Fire Tariff Shot Ahead of U.S. in Trade War

-

Najib Pleads Not Guilty to Corruption Charges in 1MDB Case By

-

China Think Tank Warns of Potential ‘Financial Panic’ in Leaked Note